.png?ixlib=gatsbyFP&auto=compress%2Cformat&fit=max&rect=0%2C0%2C680%2C680&w=680&h=680)

Key Takeaways

Cross-border payment is a type of transaction that takes place between financial institutions, businesses, and individuals, where the sender and recipient are based in separate countries.

The two main types of cross-border payments are Wholesale cross-border payments and Retail cross-border payments

Your business can greatly benefit from using cross-border payments, such as expanded customer base, control over international transactions, better exchange rates, and access to international financial services.

Banks don't have to be the only place you turn to when making international transfers. Today, It's not difficult to send money across borders using many innovative solutions.

Research confirms that the cross-border payments market value will be $290 trillion by 2030, while the current number sits at $190 trillion.

Cross-border payments offer businesses better, faster, and safer payment options in many cases. It is clear that your business can gain positive outcomes with what cross-border payments offer.

So, why is a cross-border payment considered a "global payment system"? In this post, you'll learn how cross-border payments work, their types, and benefits, and how you can apply some essential tips to help your business thrive.

Let's get started.

What are Cross-border Payments?

Cross-border payment is a type of transaction that takes place between financial institutions, businesses, and individuals, where the sender and recipient are based in separate countries.

Almost every international business that sends and receives money globally uses some form of cross-border payment.

Global cross-border transactions are expected to grow "nearly twice as fast" with a 43% increase for B2B payments, capturing worldwide international payments by 2027.

How do Cross-border Payments Work?

Cross-border transactions cover many types of payments, such as wholesale, retail, and remittances. However, this can vary among different scenarios.

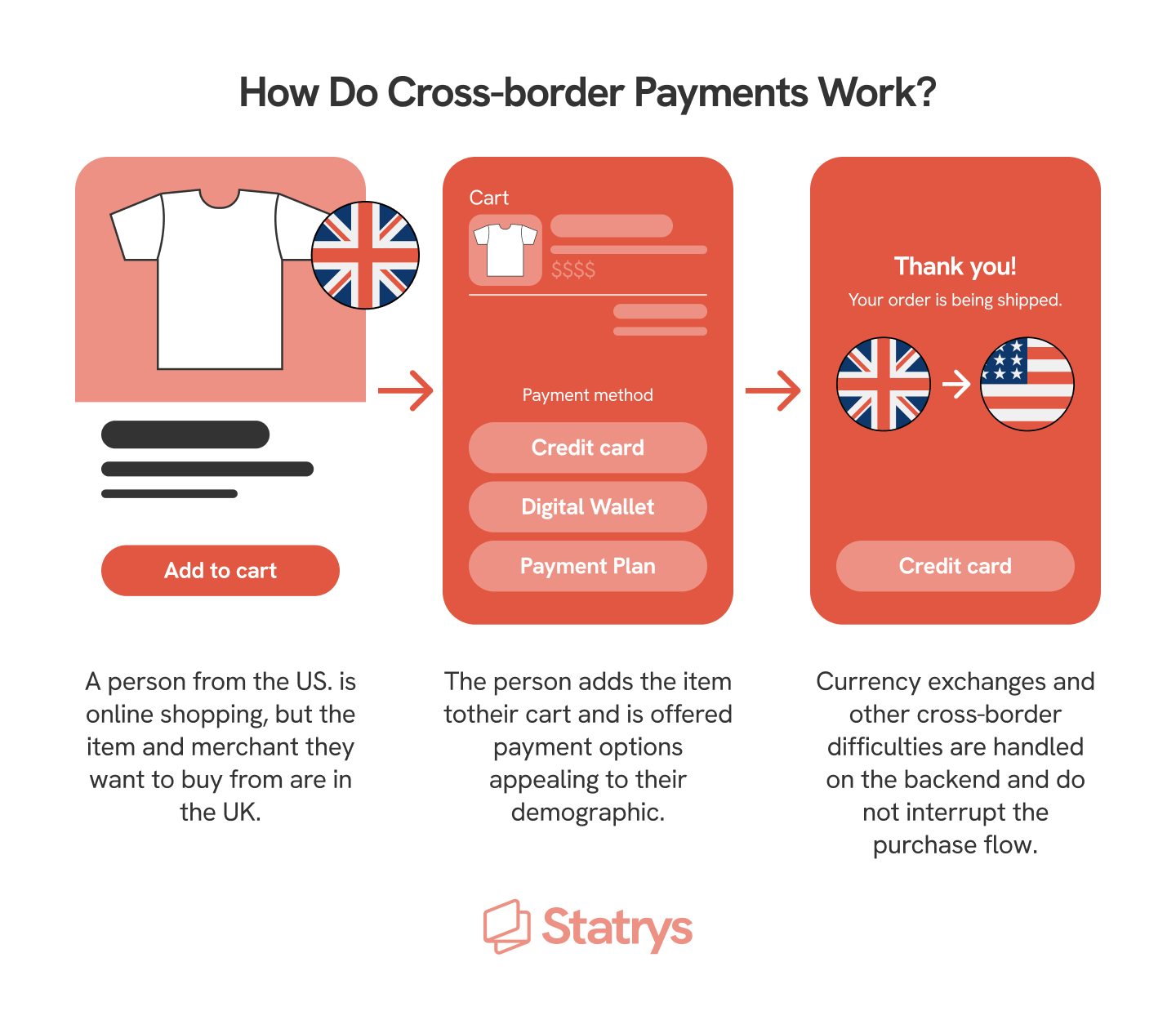

Let's look at an example of a customer in the US making an online purchase from an e-commerce store that sells clothes in the UK.

As seen above, the concept may look fairly simple. However, there are complexities to how cross-border transactions work due to several factors, including:

- Fraud prevention - Merchants can decide whether to implement localized or global fraud prevention. They can offer single and multi-authentication factors that can be set up.

- Currency exchanges - When a customer buys from another currency, there can be fluctuations from the original currency. Thus, merchants need to ensure this does not interrupt the purchase flow.

- Payment options - Based on customers' demographic, merchants should ensure their online store supports different payment options, such as credit cards, debit cards, and digital wallets.

📈 Do you manage clients and suppliers abroad? See how your business can avoid currency exchange rate risk when making international transfers

Popular Types of Cross-border Payments

Cross-border transactions represent a great solution for businesses across the world. In recent years, there are many secure online payment methods available that also support global payment platforms.

But how do you determine which type of cross-border payment function is right for your business?

Let's explore the two main types of cross-border payment:

1. Wholesale cross-border payments

This type of cross-border payment focuses on financial institutions, such as banks or in some cases financial tech firms, which typically function by supporting their own activities from one institution to another, or to support their customers' cross-border transactions.

The activities range from lending, borrowing, foreign exchange, derivatives, commodities, and securities up to trading of equity and debt.

2. Retail cross-border payments

While financial institutions support their own financial activities, this type of cross-border payment is known to be used between businesses and individuals. They include key types such as P2P (Person-to-Person) and B2B (Business-to-Business) payments.

Knowing how each type of cross-border payment functions, let's dive deeper into the examples and how each type works.

Examples of Cross-border Payments

Choosing global payment platforms that support multiple payment options will ensure compatibility with different payment currencies, exchange rates, and more.

Here are some examples of cross-border payment options and how they work:

| Types | How it works |

| International Wire Transfers |

This form of cross-border payment involves the sender providing their bank with instructions to send money to a recipient in another country, and the banks involved in the transfer facilitate the movement of funds across borders. For instance, using IBAN & SWIFT codes to transfer from one bank to another bank in a different country. |

| Global ACH Payments | These are electronic transactions, where you can transfer funds between the bank accounts within the US. ACH payments are considered as very efficient, it takes 1-2 business day for transfer to be complete and it also supports many types of payments such as direct deposit, electronic bill pyament, and POS transactions. |

| Digital Wallets | Digital wallets are also an example of a cross-border payment. Products such as PayPal, Google Pay or Apple Pay, helps to ease the transactions acorss border. However, it's important to note that digital wallets are not suitable for large transfers, rather for individual or P2P due to the transaction fees that can vary differently. |

| Credit and debit card payments | Credit and debit card payments are considered as two of the cross-border payment examples. Due to its popularity and number of usages, credit and debit cards are used almost everywhere in the world, specially for online and offline purchases. Nevertheless, one should always be wary of the fees incurred while using them due to the charges. We recommend checking with your credit or debit card's provider before making transactions. |

| Digital currencies | Digital currencies have become increasingly popular due to the amount of charges and the variety of category that you can use. some examples are Bitcoin, Litecoin, Etherum, and many more. The downside of using digital currency as a cross-border payment option is that it can be unreliable at times due to the rates and in some cases, it's unsafe to use due to fraudulent activities involved. |

| Paper checks | The classic, timeless option for cross-border payment that you can still use today. To use paper checks, all you need to do is ensure to write an accurate name of the receiver (payee) and their address to send them the check. The best thing about paper checks is that there are no fees involved in a transaction, nor any intermediary banks. But the downside of using paper checks is that it can take weeks from postal mail, and it has to be cashed. |

Benefits of Cross-border Payments

The practice of international trade has become very popular in the past few years, given technological improvements and creative innovations. Not only does this help save time and costs for individuals, businesses, and financial institutions, but it also provides more options for payments like never before.

According to BCC Research, the business-to-business segment will dominate the market as the most preferred type of cross-border transaction in 2027.

That said, there are many benefits that businesses like SMEs and other types of business can leverage from cross-border payments, such as:

- Increased control over international transactions

- Remittances are facilitated with better flows (when sending money abroad for family)

- Diversification of risks for business, operating in multiple markets

- Expanded customer base

- Better exchange rates management

- Cross-border ecommerce - opens up more opportunities for business

- Access to international financial services

These are just some of the benefits that a business can achieve with cross-border payments.

Tips for Effective Cross-border Transactions in a Business

If you're a small business, there may be several ways in which you can take advantage of your cross-border transactions. However, considering how each business is different from one another, knowing which type of cross-border payment options fit your business best would be an ideal choice.

That's why we've put together the essential tips to help you manage your business' cross-border payments effectively!

Tip #1 - Get familiar with your customer’s local payment platform

Different countries like to use different platforms to send and receive global payments. For instance, Canada and the United States prefer Paypal, whereas China almost exclusively uses WeChat Pay and AliPay

As a global business, part of your strategy should be to take these differences into consideration when accepting international transactions. Thus, it’s best to integrate their most popular systems into your checkout process.

This creates a familiar experience for your customers and saves them the inconvenience of registering for a new platform.

Tip #2 - Use a multi-currency account to handle foreign currencies

Currencies can sometimes be the underlying difference that halts your customer's payments. If your business operates on a global scale, dealing with multiple currencies is inevitable.

For this reason, it would be ideal to integrate a payment gateway or payment options that support payments in multi-currencies. Alternatively, using a business account can also be your option to start with.

For instance, Statrys Business Account supports up to 11 currencies, where you can also hold the currency in which your customers made payments, plus many other benefits from the business account.

Tip #3 - Use a secure payment system for large payments

Opt for SWIFT and CHIPS. SWIFT (Society for Worldwide Interbank Financial Telecommunication) is a secure messaging network banks and financial institutions use to exchange transaction details. Whereas CHIPS (Clearing House Interbank Payments System), managed by the Clearing House, focuses on facilitating the clearing and settlement of large-value payments, primarily in US dollars.

Think of SWIFT as a channel financial institutions use to share financial information and CHIPS as a system to confirm payment settlement.

In fundamental terms, SWIFT and CHIPS collaborate to accomplish roughly the same goal – they identify the country and bank of the person or business receiving an international payment and ensure those cross-border payments are routed correctly.

They're essential with large volume B2B transactions, where there's a lot of money involved.

Using SWIFT and CHIPS codes help to mitigate risk when conducting business with other countries and across languages, ensuring information about the receiver and the sender doesn't get lost in translation.

Tip #4 - Minimize fees with cross-border transaction fees

One of the biggest barriers to international trade for small and medium-sized businesses is global payment fees. Because most international transactions are carried out by banks, global payments have a reputation for being expensive and time-consuming.

Thankfully, with the increasing power of technology, banks are becoming less important in international payments.

More and more companies are choosing to perform their transactions through non-bank platforms like Statrys. Non-bank platforms are licensed to send and receive money just like a bank, without the heavy transaction fees. Your funds are just as safe as they are with a traditional bank.

Tip #5 - Compliance with global payment rules

Understanding global payment rules is essential. International business needs to comply with the regulations of both their own country and the country they’re doing business with.

This means twice the work is required in order to learn which laws apply to their cross-border payments process. Nevertheless, being an international business means putting in the extra time and effort to ensure you’re following all laws and regulations.

Thus, compliance with global payment rules and international laws should be one of the essential factors to take into consideration. Not only this will help you avoid issues with cross-border payments, but it will also safeguard your business from being completely ruined due to failing to comply.

Additionally, understanding the regulations will also help to prevent fraudulent or unusual activities that you may come across during international transactions.

Bottom Line

Cross-border payments work in incredible ways for businesses across the world today. It comes with many types that provide lots of options that are ideal for any type of business, and offer a better way for businesses to trade, make international transfers, and individuals to make remittances.

While it is a great option for international transfers, there are also factors that one should be aware of, such as fraud, exchange rates risks, and more. These factors can play a crucial role in the profitability of your business and therefore should be monitored closely.

However, there are always some essential tips and solutions that can help with your business. By following these tips and applying them to your business, you can be sure to make the most out of cross-border payments in a business you're in.

FAQs

Who uses cross-border payments?

Cross-border payments are used by individuals, businesses, and financial institutions that need to send or receive money across borders internationally.

What are the two main types of cross-border payments?

What are examples of cross-border payments?